Gold and inflation

21 February 2025

On the face of it, the question of whether a banking crisis and inflation (can) be fought simultaneously can be answered in the affirmative. To fight inflation, the economy must be weakened. This can be done by raising interest rates and reducing money creation.

If, for whatever reason, this leads to problems with banks, they will extend less credit. This further weakens the economy. Once inflation has fallen back sufficiently, central banks will have to reopen the money tap and cut interest rates to keep the problems at banks from getting out of hand.

So you might think that central banks should be happy with the problems in banks. After all, inflation is way too high almost everywhere, and reducing credit helps push inflation down. Unfortunately, things are much more complicated.

The big shortcoming is that central banks do not have the tools at all to fine-tune their policies in such a way that they can direct exactly how to curb inflation and credit and also time this properly; they only have very crude tools at their disposal.

In the current situation, this is very annoying because interest rates are already causing problems in the banking sector at lower levels than the interest rate level needed to properly fight inflation. Again, you might think that this need not be a big problem, because instead of being caused by even higher interest rates, the economy is now being held back by sharply declining credit, thus pushing inflation down further.

But now what if interest rate changes only affect the economy with a lag of two to six quarters anyway, and this time lag also depends heavily on how much lending declines?

This is almost impossible to predict, as the extent of problems in banks is ultimately determined primarily by confidence in the banking system. There are no models to predict this properly. Nobody knows whether confidence in banks lasts long or suddenly disappears as soon as the first problems become visible.

What is clear, however, is that if confidence really sinks significantly, governments and central banks have too few reserves to properly absorb and reverse a banking crisis. To that end, both have already shot too much of their powder since the credit crisis in 2008.

Should they now prematurely step on the accelerator again or do so too hard, this will manifest itself in rising inflation and sharply rising long-term interest rates, which could also trigger a crisis. Hence central banks have to navigate between the two extremes, but this again requires fine tuning that they cannot handle. You will therefore have to set priorities as a central bank. Do you put inflation targeting first or is preventing a banking crisis the top priority?

Moreover, the ECB and Fed make it seem as if they do not have to make this choice at all. They say they have separate tools for both problems: for inflation targeting the level of interest rates and for preventing a real banking crisis all kinds of support measures to protect account holders and banks. In theory, this is true. But in the current situation, we have our doubts.

To fight inflation properly, interest rates have to be raised further. This results in ever greater losses on banks' loan portfolios. If markets no longer trust banks as a result, governments and central banks cannot possibly prevent another crisis.

Overall, banks may be in much better shape than in 2008. However, this does not help much if one gets the impression that the loan portfolio has not only become worth less due to increased interest rates, but also because the economy is becoming so weak that many parties can no longer meet their interest and repayment obligations. To properly assess this risk, we need to look closely at what happened after the credit crisis broke out in 2008.

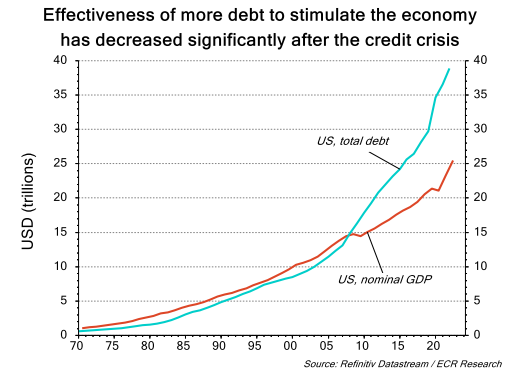

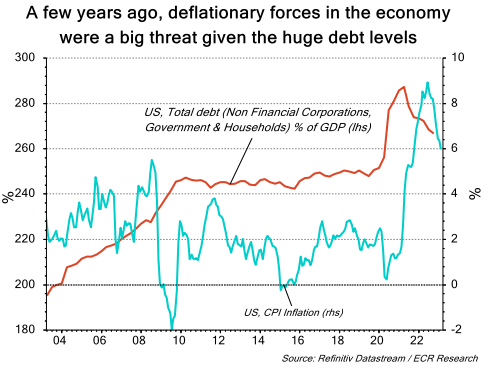

The credit crunch erupted in 2008 due to fiscal and monetary policies implemented from the end of World War II, which consistently increased debt more than the economy grew. In other words, total debt/GDP ratios kept rising. Eventually to the point where the subprime mortgage crisis left the market highly doubtful that many parties would still be able to meet their interest and repayment obligations. As a result, the entire credit card house threatened to collapse.

As this left hardly any credit, the demand side of the economy collapsed and deflation soon loomed. However, the combination of high debt and deflation is killing an economy, as the debts become increasingly heavy. So as soon as possible, the demand side of the economy had to be boosted through higher employment and wage increases.

But how to achieve this when an economic crisis and globalisation are working in exactly the opposite direction? The most obvious thing would then be to sharply increase the public deficit. In government, however, debts were already very high and, moreover, the prospect was only of even bigger deficits due to an ageing population. So the private sector had to be induced to borrow more. However, the credit crisis had started because debts there had risen too far. Understandably, then, lower interest rates in this area did not do much.

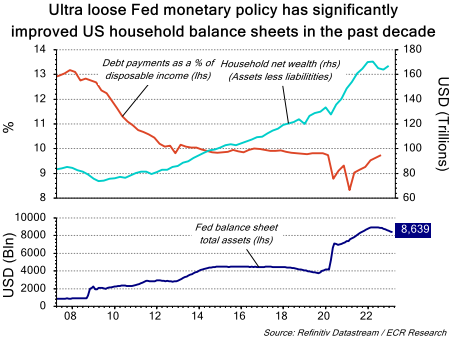

In the end, only one option remained, so-called asset inflation creation. That is, not only cutting interest rates to the max - often even to negative - but also letting the central bank create more money than the real economy can absorb (in theory, this could easily push up inflation, but this was now prevented by globalisation). The added money created then has to go somewhere.

The only remaining option was then to go to the asset markets (stocks, bonds, real estate et cetera). Soon this then drove up prices there, so that against the old debts came an increasingly higher value of assets. This in turn led to such an improvement in balance sheets that people started borrowing more again anyway. Exactly what was intended.

Nu zou het mooi zijn geweest als dit tot zoveel economische groei had geleid dat de werkloosheid er flink door zou zijn gedaald en de loonstijgingen zouden zijn opgelopen. Zo ver is het echter nooit echt gekomen:

The result was that deflation was difficult to avoid from 2009 to 2020 and economic growth remained consistently low. In addition, asset prices had been driven up far above their real underlying value by all this, so that ever lower interest rates and ever more money creation were needed to drive prices up even further. It was therefore understandable that more and more money was hoarded at the banks, for which they could find no use at all.

All this continued until early 2020, when corona turned everything upside down. Later followed by the Ukraine war. The corona crisis threatened – just like in 2008 – the credit card house to collapse. Every policymaker knew what this would mean: a very deep economic crisis. There was only one party that could prevent this: the government. Government deficits were greatly inflated. Moreover, the central banks largely financed this with money that was created extra. This created a completely new situation.

Previously, much of the extra money created remained with the banks. They had to find increasingly risky ways to still achieve returns. The same applied to all kinds of other financial institutions outside the banking world, of course. Now, the money created by the central bank ended up directly with private individuals and companies via the government. The result was that as hard as the economies collapsed after the outbreak of corona, they also recovered just as fast after a while. In other words, the demand side of the economy recovered quickly, but this did not apply to the supply side:

In other words, less supply and more demand, which turned the danger of deflation into a danger of inflation. As a result, instead of downward, upward pressure was put on interest rates.

In retrospect, the major central banks were much too slow in making the switch from fighting deflation to fighting inflation. Incidentally, in our opinion, this is not entirely to blame, because very few saw the war in Ukraine coming. This does not alter the fact that the war did lead to inflation rising rapidly to far above the targets of central banks.

If it were possible to predict that inflation would soon fall again, then there would not be much to worry about. However, the war could continue for a long time, partly because of that - and also because of broader geopolitical tensions - long-term reduced oil and gas supply, import restrictions, relocation of production from low-wage countries (particularly China) to other countries, etc.

This is also happening in a climate where the growth of the working population is decreasing rapidly, many people are still ill from Corona and/or are more susceptible to flu, there is still a lot of resistance to immigration, etc. This causes a tight labor market, so that due to the high inflation, one must be very careful of a wage-price spiral. Especially since there is still a lot of excess liquidity in the system, inflation can increase much further as a result.

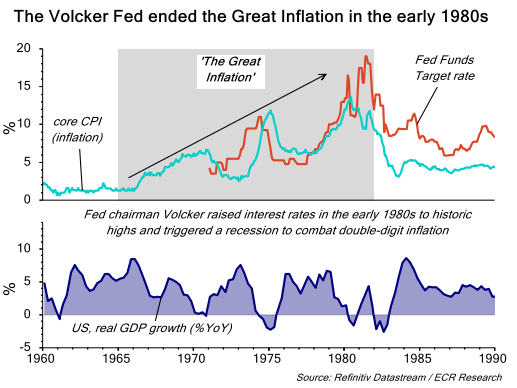

The early 80s clearly demonstrated that long-term interest rates rise to such an extent with (very) high inflation that this causes enormous economic damage. This forced Paul Volcker at the time to reduce inflation by means of high interest rates and a deep recession. It does not have to come to that now, but then the central banks must ensure a rapid weakening of economic growth and rising unemployment.

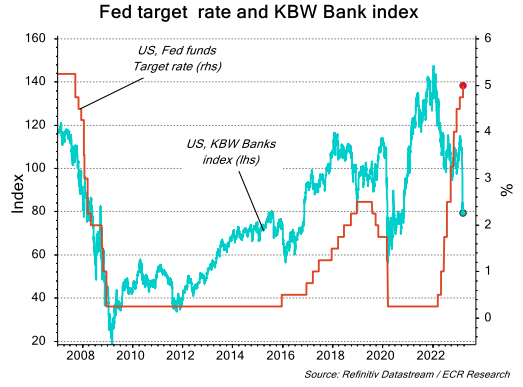

In order to prevent a wage-price spiral, the major central banks have raised interest rates at a record pace over the past year. This is now causing problems, because in the period 2009 to 2020 the short-term interest rates were 0% or even negative. As a result, bonds, shares, real estate, etc. were bought en masse with loans at a variable interest rate. The banks participated in this on a large scale by providing long-term loans and buying long-term bonds. The interest they received as a result was much higher than the variable short-term interest rates at the time. Many people really did realize that interest rates would rise again one day, but hardly anyone expected this to happen so quickly and hard.

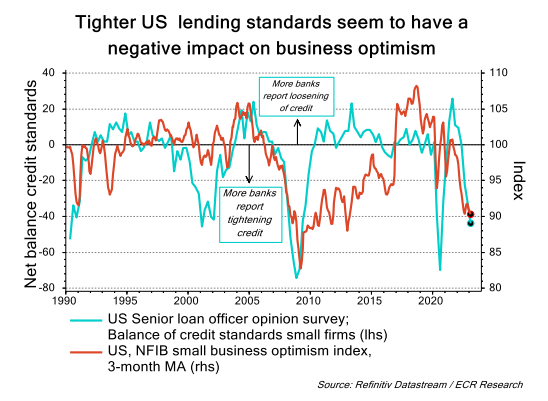

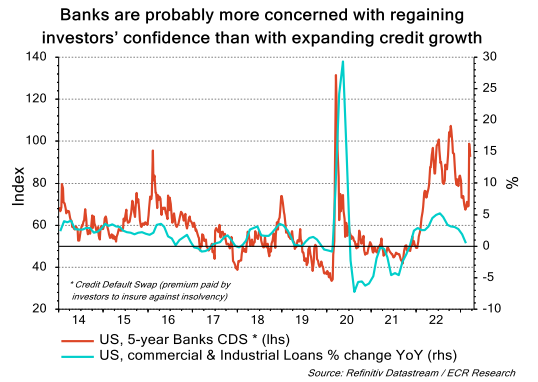

There have also been many parties that took measures to hedge against rising interest rates. However, many have also (largely) neglected to do so. In all sorts of ways, these latter parties are now confronted with losses:

Against this background, let us take a closer look at the position of the banks. Many of the banks have a large portfolio containing long-term bonds and (mortgage) loans. They finance these largely with short-term customer deposits (current account deposits, deposits, etc.). However, because a large part of their bond and loan portfolios was built up in the past, it is loss-making to finance these with customer funds on which the current much higher short-term interest rate has to be paid. That is why they only allow the interest on customer deposits to rise slowly in line with the increase in short-term interest rates.

But customers can also choose to transfer their bank deposits to money market funds. There they will receive the current short-term interest rates. Therefore, banks cannot keep the interest rates on customer deposits low for long. If customers withdraw a lot of their deposits – for example to put them in money market funds – the bank may have to sell part of its bond and loan portfolio. At current prices, this will result in a loss. Other worries for banks arise from the following points:

We would like to make two further comments on the above:

In our view, the following can be concluded from the above:

It is therefore currently very difficult for central banks to manoeuvre well between fighting inflation and preventing a banking crisis. The consequences of a banking crisis are however much worse than those of inflation remaining too high. The most practical thing is therefore to let the economy weaken slowly by means of higher interest rates and reluctance on the part of banks to provide new credit. The risk is then that too little rather than too much will be slowed down.

In practical terms, this means that in the current circumstances there is little room for further interest rate hikes. We should not forget that the previous interest rate hikes have not yet fully had their impact on the real economy (even if we take into account that many interest rates have recently fallen again). Against this background, much further interest rate hikes become far too risky. Especially since many consumers are running out of savings they saved during the corona period and there is now a negative rather than positive wealth effect.

In the scenario that we currently consider most likely, we see economic growth in the US and Europe fall back to around 0% in the coming period and gradually turn into a recession. However, we see the central banks changing course fairly quickly. As far as they are concerned, preferably when inflation has fallen to 2% or below, but also if it is still above that.

However, it does not make much difference where inflation is headed in the slightly longer term. It is as follows. Potential growth – the growth above which inflation rises at full capacity – is increasingly falling towards 1.5% in the US and below 1% in Europe. This growth is probably too low to prevent new debt problems.

The West is getting a bit of a reprieve because the weakening economic growth is now creating reserve capacity that must first be used up. So growth may be above potential for a while. However, we do not expect this to apply for a long period, because the amount of reserve capacity will be limited (as the recession is unlikely to be deep and will not last long).

Our conclusion is therefore that inflation will fall in the coming period, possibly even to 2% or below, but that it will not take long before it returns to an uptrend. We do not see the central banks taking sufficient action against this by then, because the cure will then be worse than the disease.

The Fed raised interest rates by 0.25 percentage points this week to a range of 4.75% - 5% and

indicated that it will probably raise rates by the same percentage again before

a peak is reached. In addition, Fed members predict that interest rates will probably not be cut this year;

they do not see this happening until 2024 and 2025. They therefore assume that inflation will remain too high for the time being

and that the banks will not have too many problems.

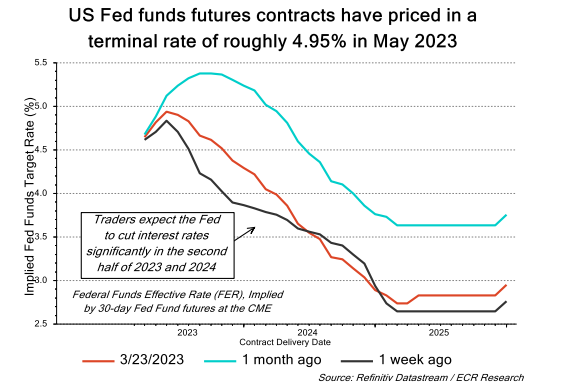

While the Fed expects a peak in interest rates at around 5.125% and then sees little or no decline this year, the markets are assuming a completely different picture. To start with, they doubt whether interest rates will be raised further, but more importantly, they expect a number of interest rate cuts this year and see this continuing next year.

That is understandable given the many comments about further expected problems at the banks (Even if the Fed were to expect this, the central bank would never publicly announce this; it would provoke the crisis itself).

We believe that – in order to combat inflation – interest rates should remain at a level for the time being at which further problems at the banks and therefore a weakening economy – later even a recession – can be expected. We therefore also expect an interest rate cut of around 0.75 percentage points later this year. We doubt whether the Fed will raise interest rates by another 0.25 percentage points before that. We expect that there will still be too much unrest around the banks for that. In particular, this concerns the question of whether the government should guarantee all deposits at banks. This would nip most of the unrest in the bud, because the ceiling for that is now $250,000, while the amounts involved are often larger.

However, we do not expect the government to go that far. That is why we see the unrest continuing and this leading to further restrictions on credit. The chance is high that this will then lead to a recession.

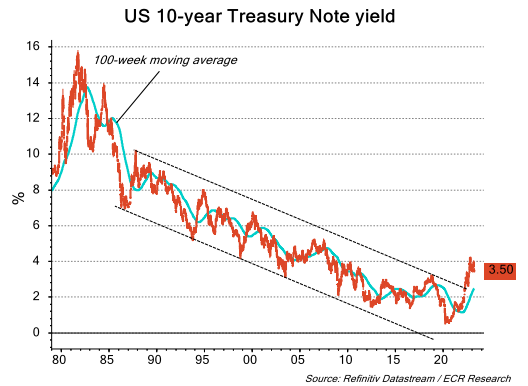

There is also not much room for long-term interest rates to rise in the US. In the event of an approaching recession, interest rates will sooner come under downward pressure. Especially in the term of 1 to 5 years, but certainly also for longer terms. We must realize that this mainly applies to loans with a high credit rating; in the event of a recession, credit spreads increase considerably.

In any case, once the 10-year US Treasury yield – currently around 3.45% – falls below 3.35%, we expect a further decline to around 2.6%. From there, we expect a sustained increase due to rising inflation.

In Europe the situation is a bit different, because the central bank there has raised the interest rate to 3%, while inflation is still well above. But the real interest rate is still negative, while due to the fight against inflation it should be at least at 0% if not positive.

The question is whether the unrest among the banks will continue in Europe and/or whether inflation will quickly fall to 3% or lower. We do see this happening, but at a slow pace. In Europe, the situation surrounding the banks seems to be better under control. That is why we see the ECB raising interest rates by 0.25 percentage points once or twice before the peak is reached and interest rates can be considered again. We therefore see European interest rates reaching a peak later than American interest rates.

In Europe, we also see interest rates being lowered later and at a slower pace. Where the bottom for interest rates will eventually be is difficult to predict now – perhaps around 2% – but after that we expect an uptrend again as a result of too high inflation.

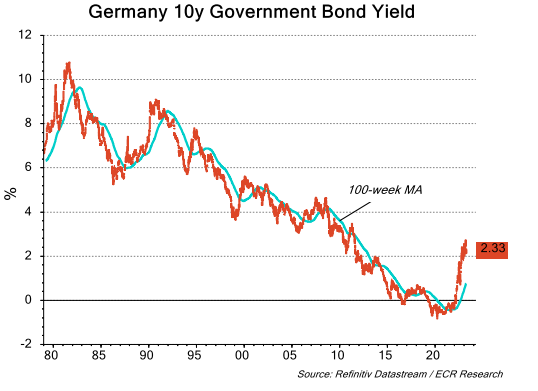

With all this, we do not expect the interest on ten-year German government bonds – currently around 2.3% – to rise much above 2.5% for the time being, unless the problems at the banks disappear completely and lending starts up again. However, we do not expect this. We therefore see the ten-year interest rate slide to around 1.8%. Incidentally, in the longer term we see the ten-year interest rate rise considerably as a result of excessive inflation.

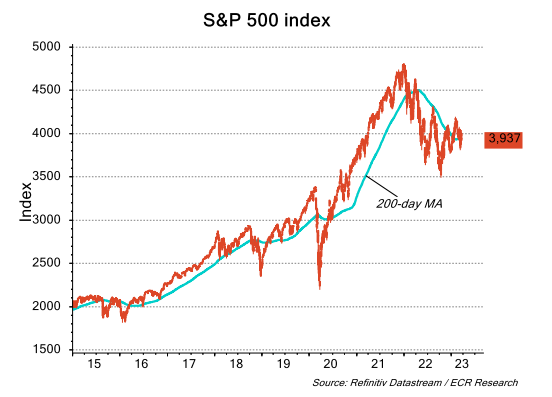

The conditions for equities are not favorable: economies are weakening towards a recession, while high inflation makes it impossible for central banks to take strong action against the weakening by stepping hard on the monetary accelerator. This does not prevent equity rallies from occurring in between. Especially because more money is now being created to help the banks.

In this constellation, we do not see the S&P 500 index rising above 4,200-4,300 – probably not much above 4,000 – and on balance sliding to around 3,300 if not lower in the coming quarters. We only see the bear market turning into an uptrend again, once central banks fear a deep recession and step on the gas again. However, it is questionable whether new peaks will be reached then, because we will then see excessive inflation increasingly playing tricks on the stocks.

We see equities in Europe performing relatively slightly worse for the time being, as we see the ECB tightening further than the Fed.

Emerging market shares may actually do somewhat better in relative terms. Lower dollar interest rates and downward pressure on the dollar are favourable for them.

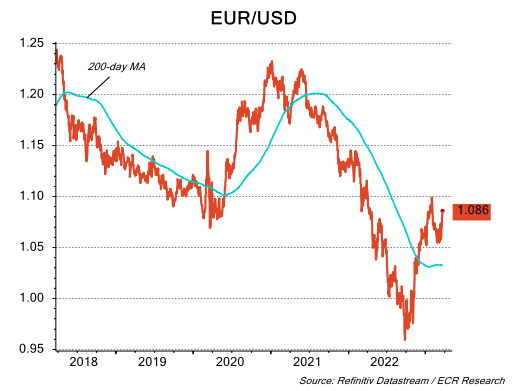

The Fed had to open the money tap for a while to absorb the problems at the banks. This has put downward pressure on the dollar. However, there is more going on. That is to say, we expect the problems at the banks to look a bit more serious in the US than in Europe in the coming period. That is why we see the ECB keeping its foot on the monetary brake for longer than the Fed. We also see this putting the dollar increasingly under downward pressure against the euro (interest rate differentials are shrinking).

On the other hand, we see stock prices falling on balance and a risk-off atmosphere is usually favorable for the US currency.

On balance, we see EUR/USD moving towards 1.15 and later towards 1.20 in the coming months to quarters. In the shorter term, however, a drop towards 1.06 and a lack of a breakout above the 1.10 – 1.12 resistance zone for the time being would not be surprising.

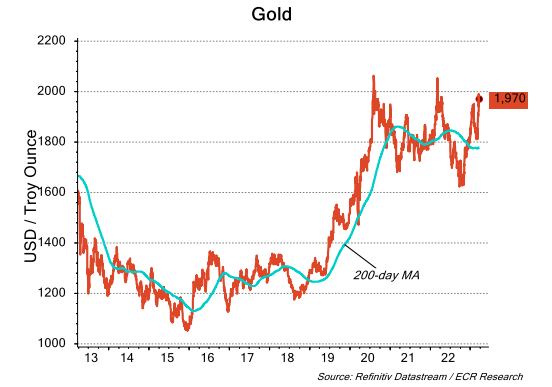

The conditions for gold have improved considerably. The high inflation is very difficult to combat due to the problems at the banks, both in the short and long term. This does not alter the fact that the economies are now sliding towards a recession, which will cause inflation to fall, but the central banks cannot yet step on the monetary accelerator. This is in principle negative for the gold price. But under these conditions, persistent problems at the banks can also be expected. This is positive for gold.

On balance, we expect a correction of the gold price to around $1880 in the short term, but we see the price rising to around $2400 in the coming year and later to around $3000. In any case, a breakout above $2100 would be very positive.

Other inflation hedges – other precious metals, real estate, commodities and the like – we see basically following the pattern of the gold price. However, commodities and commercial real estate are more sensitive to the economic slowdown in the coming period.

Do you have any questions about this report? Or about developments in the financial markets? Or about your risk management in the broadest sense? Please contact our independent interest rate, currency and commodity advisors. By phone at 030-8201221 or by email icc@icc-consultants.nl.

Disclaimer: Statements and opinions expressed in this blog/column are the personal opinions of the author and/or guest bloggers. These are separate from any official positions of persons, companies or organizations, or companies and organizations that are explicitly mentioned in the published blogs & texts.

Director and owner

Be the first to discover the latest products and the latest news about precious metals.

Be the first to discover the latest products and the latest news about precious metals.